Backtest with Tick Data Suite

Backtesting is a crucial step in the development and evaluation of trading strategies. It allows traders to assess the performance and effectiveness of their strategies by simulating past market conditions. An essential tool for this process is the Tick Data Suite (TDS), which offers comprehensive backtesting that considers various factors such as swap costs, slippage, and trading costs. In this article, we will discuss how TDS, combined with high-quality Dukascopy data, enables accurate and reliable backtesting to help traders optimize their strategies. Combining Tick Data Suite’s high-precision backtesting with Quant Analyzer’s robust portfolio analytics offers an in-depth view of an Expert Advisor’s risk profile and profit potential. This synergy enables traders to make data-driven decisions by scrutinizing performance under realistic market conditions and examining key risk metrics.

Tick Data Suite is an advanced backtesting software that facilitates the process by accounting for several critical factors, including swap costs, slippage, and trading costs. This comprehensive approach ensures that the backtesting results are as close as possible to real-life trading scenarios. TDS also allows traders to perform scam tests, which fool the Expert Advisor (EA) with manipulated dates to evaluate its response to potential discrepancies.

Using Dukascopy Data to Ensure 99.9% Modelling Quality for Backtests

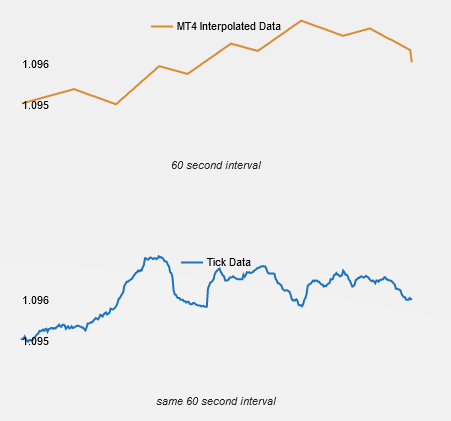

To achieve the utmost accuracy in our backtests, we rely on Dukascopy data, which boasts a 99.9% modeling quality. This Swiss-based forex broker provides comprehensive historical data for various financial instruments, ensuring the reliability of our backtests. When backtesting with tick data, MetaTrader 4 solely relies on a random simulation of ticks. However, an interpolation process is employed using both bar price data and tick count to produce prices for each tick. The disparity between interpolated data in MetaTrader 4 and actual tick data is depicted in the accompanying image.

In addition to Dukascopy data, we employ the ‘every tick’ model to simulate real trades as closely as possible. This approach accounts for each price movement, resulting in highly realistic trade simulations and improved backtesting results.

The hardware we use

At EA Analyzer, we prioritize the accuracy of historical data for evaluating Expert Advisors (EAs), well aware that the integrity of this data is crucial for reliable analysis. Our setup features a high-performance computer equipped with ECC (Error-Correcting Code) memory and powered by a Xeon processor. This combination is essential, especially considering that the data for just one currency pair over the span of a year can encompass between 6-9 million ticks. The role of ECC memory is indispensable in this context; it ensures the precision of every tick by automatically detecting and correcting any errors. This meticulous approach to maintaining data integrity is vital, as even minor inaccuracies can lead to incorrect assessments of an EA’s performance. By relying on our system, traders are equipped with the most accurate and reliable historical data possible, allowing for the informed evaluation of EAs.

The 28 year shift to the past

Some Expert Advisors (EAs) are designed to trick the backtest results to look better. They can do this by setting specific dates or times that affect the results. For example, an EA might not trade during periods when it usually loses money, or it might start trades only on certain dates it’s programmed to recognize. Sometimes, an EA avoids trading on specific ‘blacklisted’ dates.

However, there’s a reason why an EA might skip certain dates on purpose. If an EA avoids trading during big news events in real life, it might skip these dates in backtests too. This is a valid strategy, but it’s hard to set up, and many EA developers don’t do it.

One common way to test if an EA is cheating is by shifting the backtest data by 28 years. This keeps the days of the week the same, which is important for accurate testing. If you shift by a different amount, like one year, you’ll get incorrect trading times and other errors.

In theory, you could shift the data 28 years into the future, but this could lead to issues in 2038 due to the y2k38 problem, where computer systems might struggle with the time representation.

If an EA is honest and doesn’t have hardcoded dates, the backtest results should be nearly the same, whether you shift the data by 28 years or not. Remember, if an EA skips dates for news events in live trading, it might do the same in backtests. This can be a good indicator of whether the EA is reliable or trying to cheat the tests.